The United States remains a top destination for global real estate investors due to its stable legal system, strong property rights, and high potential for appreciation in key markets. In 2026, the process of securing financing for a Foreign National (investor without US citizenship or permanent residency) remains viable but requires stricter compliance and more capital than domestic loans.

The “Service of Process” Requirement

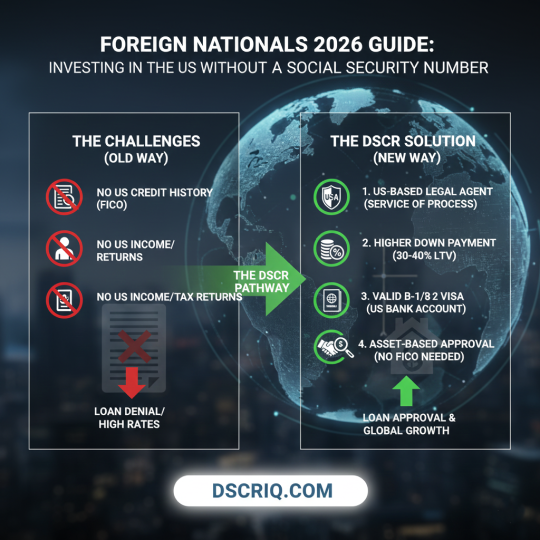

Lenders financing foreign-owned property have tightened legal requirements to ensure they can execute legal actions, if necessary, without relying solely on international courts.

- US-Based Legal Agent: Many major lenders now require the foreign borrower to designate a dedicated Service of Process Agent who resides in the US. This individual or firm is legally authorized to accept official loan correspondence, default notices, and court documents on behalf of the borrower.

- Distinction: This is a key distinction from a standard Registered Agent (often required for an LLC), as the service of process agent is directly related to the mortgage agreement and facilitates communication between the lender and the non-resident owner.

LTV Standards: Capital Reserves are King

Since the foreign borrower’s financial history and primary residence are outside the US jurisdiction, lenders mitigate risk by demanding a larger capital cushion.

- The Standard Down Payment: While domestic investors can access up to 75% LTV (25% down) on investment properties, the standard requirement for Foreign National loans in 2025 is a minimum of 30% to 40% down payment (60% to 70% LTV maximum).

- Asset Strength: The primary underwriting focus shifts entirely from income to asset verification. Lenders want to see the down payment and required reserves sourced from stable, verifiable international banks, often requiring 12 months of statements and notarized translations if the funds are not denominated in a major currency.

No Credit? No Problem: Asset Strength Over History

The primary barrier for foreign investors used to be the lack of a US credit history (FICO score). Specialized lenders have largely solved this by pivoting their focus.

- International Credit Reports: For investors from countries with sophisticated credit systems (e.g., Canada, UK, Australia, Germany), lenders can utilize third-party services to generate an “International Credit Report” that translates local credit history into a US-compatible format.

- The True Focus: For all others, the lender simply waives the credit requirement entirely in favor of robust asset verification. The large down payment (30-40%) combined with the required liquid reserves serves as the primary gauge of the investor’s financial strength and reliability.

Visa Check: Establishing a US Nexus

While a Green Card or US work visa (H-1B, L-1) is not required for investment property financing, basic US residency ties are usually necessary to facilitate the financial transaction itself.

B-1/B-2 Requirement: A valid B-1 (Business) or B-2 (Tourist) visa is often the minimum requirement necessary to legally travel to the US and establish the banking relationship needed for closing the loan. This acts as the essential first step in creating a verifiable financial connection to the country.

The Bank Account Requirement: To fund the loan and manage local expenses, you must have a US bank account in your name. To open this, most banks require the borrower to be physically present and have a valid visa.